[비즈한국] The financial sector is buzzing as KB, Shinhan, and Woori Financial Group316140 have issued a joint statement regarding the contents of their annual reports filed with the U.S. Securities and Exchange Commission (SEC). It was confirmed that the three companies identified their participation in government financial policies, such as inclusive finance, as potential risk factors that could negatively impact their financial status. While they explained that this was merely reflecting risk factors in accordance with the characteristics of the U.S. disclosure system and not intended to discriminate against domestic investors or criticize government policy, the discrepancy with their domestic stance is causing a stir.

On May 15, KB, Shinhan, and Woori Financial Group made an unusual joint statement. This followed the realization that their 2025 annual reports (Form 20-F) submitted to the U.S. SEC in late April identified participation in productive and inclusive finance policies—the core financial agenda of the Lee Jae-myung administration—as an investment risk. These details were not included in their domestic business reports.

The three companies explained, "Due to the nature of the U.S. disclosure system, there is a difference in that potential risk factors and uncertainties must be disclosed broadly," adding, "We are not providing additional information to specific investors or discriminating against domestic investors." KB, Shinhan, and Woori have issued and listed American Depositary Receipts (ADRs) on U.S. exchanges; among the four major financial groups, Hana Financial Group is not listed in the U.S.

According to the 2025 20-F forms submitted to the SEC by KB, Shinhan, and Woori, all three companies stated under their "risk factors" section that: "We may be required to provide loans to small and medium-sized enterprise (SME) borrowers that we would not typically provide, or to provide loans under conditions we would not otherwise offer, as a result of participating in government-led projects." They also noted, "Such government policies could have a significant negative impact on our financial condition and operating results."

The three companies also identified inclusive finance policies as a factor that could deteriorate financial soundness. KB and Shinhan Financial stated, "The government has pursued inclusive finance policies to improve financial accessibility for low-income or financially vulnerable borrowers by encouraging banks to provide preferential loans. Efforts to comply with these policies may require adjustments to business practices, which could ultimately lead to an increase in delinquency rates and a deterioration of asset quality."

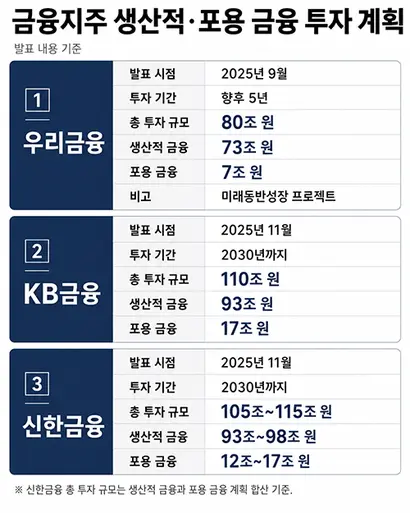

Woori Financial cited its plan announced last January to invest up to 7 trillion won in inclusive finance over the next five years, stating, "Government policies may require us to provide financial support to sectors we would not normally support, which could lead to us incurring unintended costs or losses."

In response, KB, Shinhan, and Woori explained that identifying government policies and regulations as risks is a standard practice under U.S. disclosure regulations. In their statement, the three companies noted, "U.S. disclosures require the comprehensive listing of various possible scenarios for investor protection and to defend the issuer's legal liability," adding, "The U.S. SEC manages the impact of government policy changes on a company's business and financial condition as one of its key inspection items."

The three financial groups likely issued a joint statement to preempt criticism that their disclosures contradicted their prior actions regarding productive and inclusive finance. Since the inauguration of the current administration, financial authorities have held meetings on the "Great Transformation of Productive Finance" and "Great Transformation of Inclusive Finance," urging the participation of financial companies, related institutions, associations, academia, and industry experts. Consequently, all three companies have planned large-scale investments or announced related programs in line with government policy.

Woori Financial announced its "Future Co-Growth Project" in September 2025, which involves investing a total of 80 trillion won (73 trillion won in productive finance, 7 trillion won in inclusive finance) over five years. In November 2025, KB Financial and Shinhan Financial announced plans to invest a total of 110 trillion won in productive and inclusive finance by 2030. KB Financial plans to inject 93 trillion won into productive finance and 17 trillion won into inclusive finance, while Shinhan Financial plans to inject 93–98 trillion won into productive finance and 12–17 trillion won into inclusive finance.

As such, KB, Shinhan, and Woori emphasized that their management direction was set according to government policy. The three companies stated, "We are continuously striving to contribute to economic development and the expansion of the social role of finance by increasing financial accessibility for common people, small business owners, and SMEs, and by strengthening the supply of funds to venture, new industry, and real economy sectors. We are participating in these policies voluntarily. Each company's credit systems are designed and operated according to internal risk assessments and systematic risk management, and we are proceeding with full consideration of the long-term benefits derived from maintaining a sound financial system."

Industry observers believe that, given the U.S. market environment where litigation against corporations is frequent, the companies were compelled to specifically document even policy risks. Furthermore, the rising trend in the average delinquency rate for SME loans among the four major commercial banks (KB Kookmin, Shinhan, Hana, and Woori), which rose from 0.41% in Q4 2024 to 0.45% in Q4 2025 and 0.53% in Q1 of this year, is cited as a background for why financial companies identified productive and inclusive finance policies as factors for worsening soundness.

Expert opinions are similar. Lee Jung-hwan, a professor at Hanyang University's College of Economics and Finance, pointed out, "Compared to existing portfolios, delinquency rates can rise when corporate lending increases. While financial firms will manage their delinquency rates, it is true that corporate loans have higher insolvency rates than household loans, so it can certainly be considered a risk factor."