[비즈한국] SK Hynix000660 has achieved its highest-ever quarterly performance in the first quarter of this year, recording an operating profit margin of 72%. Driven by a surge in demand for artificial intelligence (AI) semiconductors, revenue exceeded 50 trillion won for the first time in history, while operating profit nearly doubled compared to the previous quarter. Despite the first quarter typically being considered an off-season, the company achieved exceptional results in both sales and profitability. The primary factor behind these results is the increased proportion of high-value products, centered on High Bandwidth Memory (HBM).

On the 23rd, SK Hynix disclosed its consolidated first-quarter management performance, reporting 52.5763 trillion won in revenue, 37.6103 trillion won in operating profit, and 40.3459 trillion won in net profit. Revenue surpassed 50 trillion won for the first time in a single quarter, and both operating profit and operating profit margin (72%) are the highest since the company's founding. Operating profit nearly doubled from the previous quarter, marking a notable improvement in profitability.

This performance is considered an 'earnings surprise' that exceeds market expectations. In particular, an operating profit margin exceeding 70% is an exceptional level even when compared to major global big tech companies. It surpasses not only Samsung Electronics005930 (43%) but also global semiconductor giants Nvidia (65%) and TSMC (58.1%). This is analyzed as a result of increased sales of high-profit AI memory products such as HBM, alongside a sharp rise in DRAM and NAND prices.

A clear shift in supply and demand lies behind these results. Kim Woo-hyun, Chief Financial Officer (CFO) of SK Hynix, explained in a conference call that day, "Although the first quarter is typically a seasonal off-season, the strong demand from expanded AI infrastructure investment offset this, leading to a continued tight supply environment. In particular, server DRAM and enterprise SSDs led the price increases."

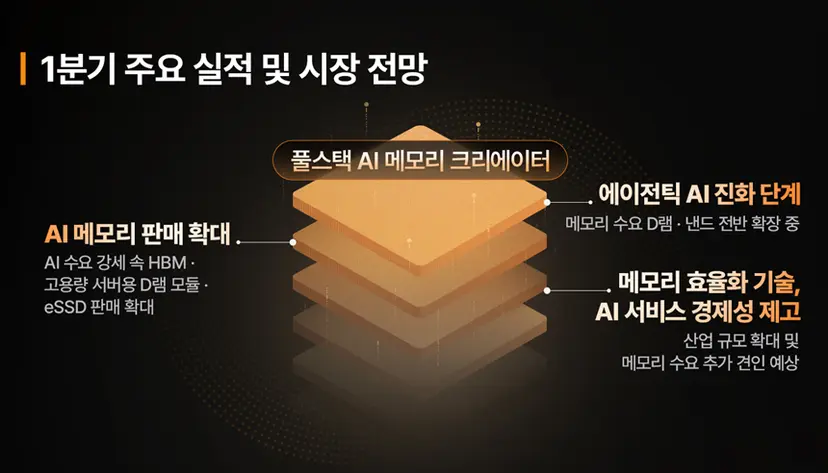

Indeed, analysts suggest that the expansion of AI server investment is changing the very structure of memory demand. As the industry shifts from large-model training to real-time inference and agent-based services, data processing volume is surging, leading to demand spreading beyond just HBM to server DRAM and high-performance SSDs overall. Memory efficiency technologies are also seen as creating a virtuous cycle that promotes service scaling and, consequently, boosts total demand.

This trend has also been reflected in prices. The company's view is that the current rise in memory prices is not a short-term rebound, but a structural change. During the conference call, SK Hynix stated, "As the importance of memory grows with the advancement of AI technology, customers are prioritizing securing volume over price. As supply expansion takes time, the favorable price environment is expected to continue for the time being."

The financial structure has also improved rapidly. As of the end of the first quarter, cash and cash equivalents stood at 54.3 trillion won, an increase of 19.4 trillion won from the previous quarter, while borrowings decreased to 19.3 trillion won. As a result, the company secured 35 trillion won in net cash, significantly increasing its investment capacity.

Based on these secured funds, SK Hynix plans to accelerate the expansion of its production capacity. Its strategy is to strengthen its mid-to-long-term demand response capabilities through infrastructure investment centered on the Yongin Cluster and Cheongju M15X fab, as well as the procurement of EUV equipment. The company maintains its stance of proactive investment, particularly because supply stability is directly linked to competitiveness in the AI era.

The company is also accelerating the reinforcement of its product competitiveness. In the HBM field, it plans to maintain market leadership based on comprehensive technological capabilities, including not only process technology but also TSV packaging.

Next-generation DRAM and NAND products will also be introduced sequentially. Hynix plans to respond to overall AI demand by expanding its product portfolio, including LPDDR6 with 10-nanometer 6th-generation process technology, high-capacity server DRAM modules, and 321-layer QLC-based SSDs. Strengthening QLC SSD competitiveness through collaboration with Solidigm is also a key strategy.

However, burdens due to rising prices are being detected in some traditional demand areas such as PCs and mobile. Analysis suggests that signs of short-term demand slowdown are appearing due to shipment volume adjustments by set manufacturers and changes in product mixes. Nevertheless, the prevailing view is that the overall memory market's growth will be maintained as server-centered demand offsets these factors.

Market forecasts are also relatively optimistic. Although suppliers have resumed new fab construction and infrastructure investment, it is expected that a significant amount of time will be required for actual expansion of production capacity (Capa).

The industry is paying attention to the fact that the memory demand structure is changing fundamentally as AI technology evolves from large-model training to the 'Agentic AI' stage, where real-time inference and decision-making are performed. As data processing increases, the total memory required across systems, including HBM, server DRAM, and eSSD, is rapidly expanding. Analysts suggest that with such structural demand expansion and supply constraints coupled, the memory market cycle is likely to show a different trend than in the past.

CFO Kim stated, "In the HBM business, execution capabilities that integrate performance, yield, quality, and supply stability are the core competitive edge. We plan to expand the volume of HBM4 according to schedule by collaborating with customers from the initial stage."