The Strait of Hormuz in the Middle East, the core heart of global maritime trade and the most vulnerable bottleneck for global energy transport, has finally reopened its sea lanes. With the United States and Iran dramatically signing a peace agreement in Switzerland centered on the full reopening of the Strait of Hormuz, the flames of war that had engulfed the Persian Gulf have temporarily ceased. Since the announcement of the agreement, the maritime logistics network appears to be rapidly recovering, with the weekly cumulative number of transiting vessels increasing by over 168% and crude oil shipments through the long-closed strait surging by 1,218.8% compared to the previous week.

However, global shipping companies and major nations, having painfully experienced the fact that a core choke point of the global supply chain could be paralyzed in an instant during this war, are moving away from the existing logistics structure that was entirely dependent on the Persian Gulf, even after the strait's reopening. To respond to the shockwaves of the Hormuz blockade that battered the world during the crisis, multidimensional efforts to seek detours—such as routes around the Cape of Good Hope in Africa, Middle Eastern land pipelines, and alternative transshipment networks originating from India—are continuing, reshaping the global logistics map.

The Strait of Hormuz is the maritime gateway through which oil-producing countries along the Persian Gulf—such as Saudi Arabia, the United Arab Emirates (UAE), Kuwait, Iraq, and Qatar—export energy to the global market. Examining the physical structure of the strait, the narrowest passage is only about 39 km wide, and the actual route where Very Large Crude Carriers (VLCCs) can safely navigate is limited to a narrow 3.2 km wide channel.

For this reason, it is classified as the world's largest maritime bottleneck where the risk of transit blockage is maximized whenever a geopolitical shock occurs. The fact that approximately 25–34% of global seaborne crude oil volume and about 20% of LNG trade pass through this strait illustrates that instability in this region directly leads to a disruption in the global energy supply chain.

Historically, the Strait of Hormuz has been a focal point of international political and economic conflict. During the so-called 'Tanker War' in the 1980s, when both sides indiscriminately attacked each other's oil facilities and tankers during the Iran-Iraq War, the risk of transit in the strait became extremely high, leading to a spike in international oil prices and a contraction in global trade volume.

The blockade following the recent U.S.-Iran war also perfectly reproduced the supply shocks of the past. Immediately after the outbreak of the war, the number of vessels passing through the strait plummeted by 90–95% compared to normal times, dropping to a level of about one vessel per day, and this led to a 45.9% collapse in cargo handling at the UAE's Jebel Ali Port, a core logistics hub in the Middle East.

Although the reopening is underway due to the peace agreement, international oil prices, including Dubai crude and West Texas Intermediate (WTI), soared past $100 per barrel at closing during the blockade period. This resulted in maximizing cost-push pressures for energy-intensive industries such as domestic oil refining (23.5%) and power/gas (20.2%).

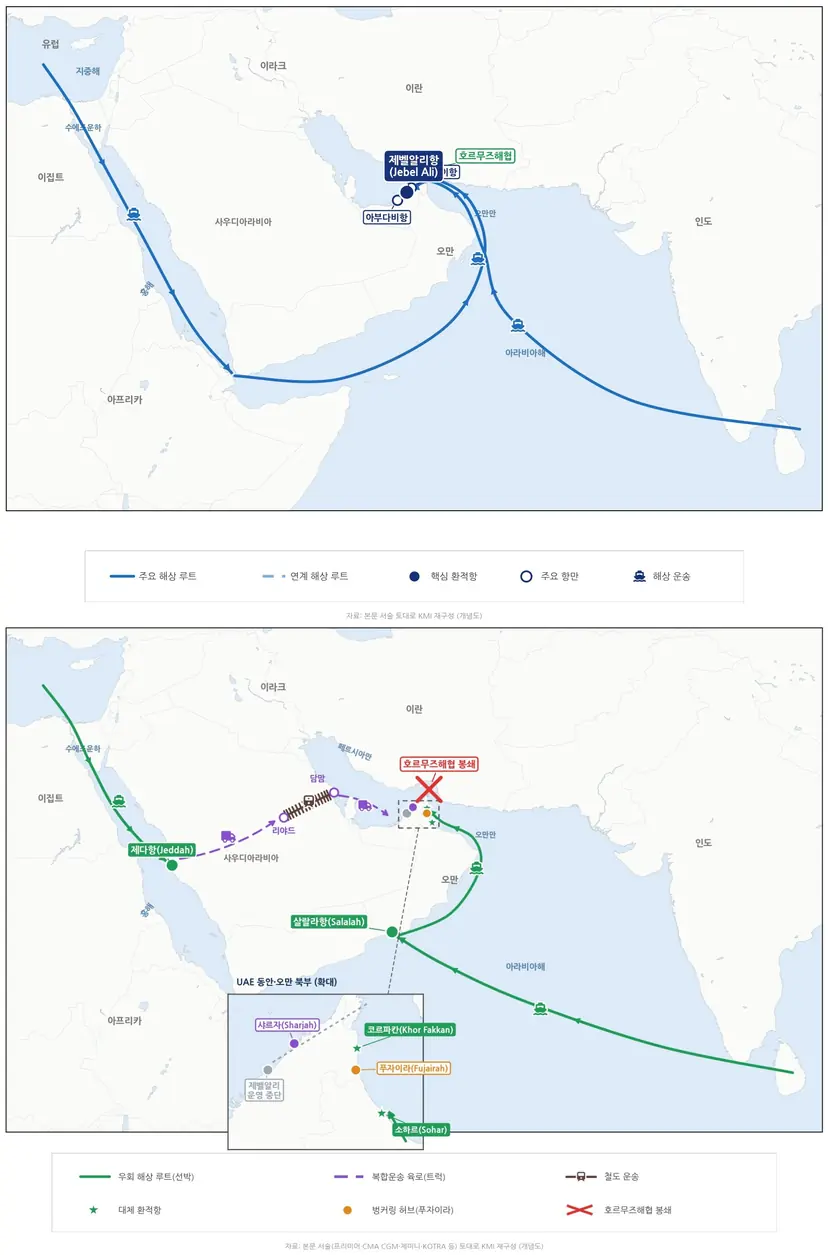

Detouring via the Cape of Good Hope Instead of the Strait of Hormuz

Amid the blockade of the Strait of Hormuz and the sequential instability of the Red Sea, the most definitive maritime alternative chosen by global shipping companies was the route bypassing the Cape of Good Hope at the southern tip of Africa. Mega-shipping lines that dominate the global market, such as MSC, Maersk, Hapag-Lloyd, and CMA CGM, officially adopted the Cape of Good Hope route as their strategy for liner services instead of the existing Suez Canal route to avoid the danger of entering the Persian Gulf.

However, this detour route comes with massive distance and time losses. Based on routes from Asia to Europe, the sailing distance increases by up to 11,000 nautical miles (approximately 20,372 km), and the time required also increases by an average of 10 to 20 days compared to normal times, and up to a month in cases of adverse weather, causing logistics delays.

The sharp increase in sailing distance caused a surge in ship fuel consumption and stimulated 'Ton-mile' demand—a concept in the shipping market multiplying cargo volume by transport distance—exacerbating the shortage of vessel capacity. To compensate for the soaring fuel and operational costs, shipping companies began imposing war risk surcharges and Emergency Fuel Surcharges (EFS) of up to $1,500 to $2,000 per container. Furthermore, as global insurance markets like Lloyd's of London canceled war insurance coverage for the Persian Gulf or temporarily increased hull insurance premium rates to 3%, a level 12 times higher than before, the burden of maritime transport costs spread across the board.

The normalization of such long-distance detour routes has also changed the landscape of the maritime refueling (bunkering) market. As the functionality of the Port of Fujairah in the UAE, a core bunkering base in the Middle East, weakened, diverted vessels flocked to the African coast. Consequently, Port Louis in Mauritius, Walvis Bay in Namibia, and the Port of Tema in Ghana have emerged as new hubs for refueling and ship maintenance, enjoying the reflexive benefits of the supply chain shift.

The Pros and Cons of Operating Land Pipelines: Detour Capabilities and Weaknesses of Middle East Pipelines

In response to the paralysis of maritime transport, the land crude oil pipeline networks owned by Middle Eastern oil-producing countries were also mobilized as key detour routes. The most representative infrastructure is the 'East-West Pipeline' owned by the Saudi state-owned oil company Aramco. This pipeline starts from the oil fields in the eastern part of Saudi Arabia, inside the Strait of Hormuz, crosses the continent, and can transport up to 5 million barrels of crude oil per day to the Yanbu Terminal on the Red Sea coast, outside the boundary of the strait.

Another route is the Abu Dhabi Crude Oil Pipeline (ADCOP) in the UAE, which connects crude oil from inland oil fields directly to the Port of Fujairah on the coast of the Gulf of Oman, outside the Strait of Hormuz, providing a transport capacity of 1.5 million barrels per day. As maritime routes were blocked, demand for alternative routes soared; for example, the Yanbu Port, which handled about 1.27 million tons of cargo before the crisis, saw its volume jump to 4.21 million tons in June, making maximum use of the detour pipeline.

However, these pipelines have clear capacity limits in fully replacing maritime cargo volumes. While the existing crude oil volume transported through the Strait of Hormuz reaches an average of 20 million barrels per day, the total capacity that can be diverted by maximizing the Saudi and UAE pipelines combined is only 3.5 to 5.5 million barrels per day. Since it can only handle about one-fourth of the total volume of the strait, it is impossible to completely bridge the structural supply deficit.

Moreover, in the case of the Saudi Yanbu Terminal, which has the largest detour capacity, its final destination is located on the Red Sea coast, exposing it to the security vulnerability of drone and missile attacks from the Houthi rebels in Yemen. This clearly demonstrates the limitation that land detours are also not free from other geopolitical risks.

Lee Eon-kyung, Head of the Shipping, Logistics & Maritime Research Division at the Korea Maritime Institute, said, "The UAE plans to increase the capacity of the ADCOP from the existing 1.5 million barrels to 3 million barrels by 2027, and the Iraq-Türkiye pipeline is also pushing for an expansion from 200,000 to 800,000 barrels. Middle Eastern oil-producing countries that must export their crude oil are embarking on new pipeline expansions as a self-rescue measure." She added, "However, there is a limitation in that there is no way to transport LNG (Liquefied Natural Gas) or general container cargo through oil pipelines."

Paralysis of Hub Ports and Cargo Shift: The Rise of India and IMEC

As the war restricted direct liner calls at the UAE's Jebel Ali Port, the hub port in the Persian Gulf, shipping companies began establishing transshipment systems using alternative ports outside the threatened waters. Shipping companies utilized ports like Sohar and Salalah in Oman, Khor Fakkan in the UAE, and Jeddah in Saudi Arabia as detour unloading hubs, operating multimodal logistics systems that combined feeder vessels (small coastal ships) and land truck transport.

The congestion and spread of risk in major Middle Eastern ports triggered a shift in cargo volume to nearby Asian ports. As cargo from Asia bound for the Middle East and Europe was urgently diverted to Nhava Sheva and Mundra ports, the western gateways of India, side effects such as a sharp increase in the number of vessel waiting days (congestion) and the intensification of bottlenecks in inland logistics were observed.

The Indian government is taking this cargo shift as an opportunity to expand its domestic port infrastructure. It is pursuing a mid-to-long-term strategy to intensively develop ports like Vizhinjam, located in the southern region, as an emerging alternative transshipment hub capable of accommodating mega-container ships.

Along with these measures to diversify maritime routes, the need to pioneer the 'India-Middle East-Europe Economic Corridor (IMEC)' has emerged as an alternative to fundamentally resolve supply chain risks. IMEC is a large-scale multimodal transport network that connects from western Indian ports by sea to the UAE, passes through an inland rail network traversing Saudi Arabia, Jordan, and Israel, and then connects by sea to Europe. It is attracting attention as a long-term detour card that can ensure the stability of Eurasian trade even if similar geopolitical risks recur in the future, as it can simultaneously bypass the maritime choke points of the Strait of Hormuz and the Suez Canal.

Director Lee Eon-kyung explained, "Analyzing cargo volume data, we confirmed that the cargo volume of ports on the IMEC route—such as Mundra Port in India, Colombo Port in Sri Lanka, Jeddah Port in Saudi Arabia, and Haifa Port in Israel—increased significantly after the crisis." She added, "This shows that IMEC played a role in absorbing detour demand during the crisis situation."